If you were to Google any topic about “understanding credit” right now, you would be directed to over 9 billion hits in total. That is an unfathomable amount of information to try and sift through. On top of that, you may not be able to tell what information is reliable and what information is misleading.

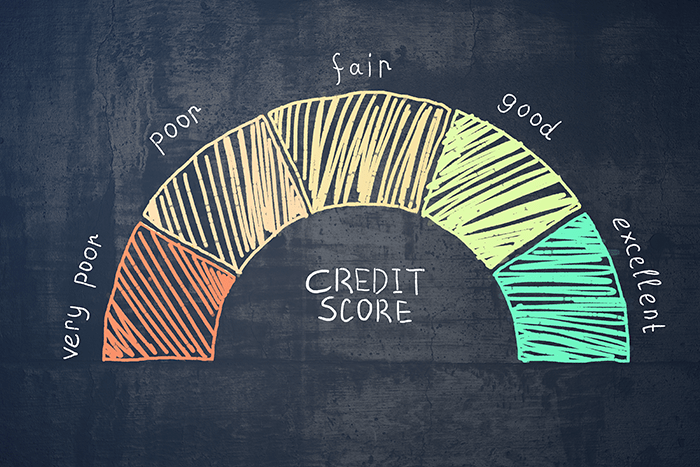

Credit is one of the most important topics related to finances that will consistently affect a person’s financial situation. It is crucial to know what information to trust especially when it comes to building, maintaining, and using your credit wisely. Your credit score is a personal 3-digit number that fluctuates for many different factors (that we will discuss later in this article). These scores range from 300 to 850 being the highest credit score you can achieve.

So where can you go to find reliable sources? How can you understand credit with SO much information out there? This article aims to answer your questions and provide additional information about understanding credit.

Why is Credit Important Anyway?

Everyone cares about your credit score! Like many people who are just starting to build credit, you may not understand the scope of what a credit score does for your future. When we say everyone cares about your credit, we mean that credit scores will be used by Banks, Credit Unions, Insurance Companies, loans, credit cards, etc. Your personal 3-digit score is built on credit history, which takes time to maintain and rebuild. Lenders use your score to determine the likelihood you will repay a loan or credit card statement. These 3-digits hold a lot of power over spending limits, types of credit card perks you can have, types of loans you can get, and approval/rejection of all of these things.

Loans and credit cards matter for different reasons. You may need loans for educational purposes, house payments, car payments, business startups; you can pretty much search for a loan for most major financial needs in life. Getting approved for a loan is greatly impacted by your credit score which is greatly impacted by credit card usage and payments. The higher your score is, the lower the interest rates will be.

Obtaining additional credit at preferred rates is also heavily based on your credit score. Insurance will look at these rates and some employment opportunities may take a peek at the score too. Lenders look at many other factors in your life including length of employment, debt responsibilities, child support, capital assets (how much you have in retirement savings and non-retirement savings), ability to repay the loan, and purpose for the loan. Although these things don’t affect your actual credit score, they are still taken into consideration when it comes to understanding YOU and your credit responsibilities.

Credit can be an overwhelming topic. It can even be discouraging if you have a lower credit score and are not sure how to improve it. But it shouldn’t be something you should be scared of! There are plenty of approachable, reliable sources you can reach out to.

What Affects a Credit Score

If you take a look at the graphic above you can see the main factors that make up your credit score. To break down the chart of what affects your credit score, we must talk about the things that aren’t explicitly explained.

What hurts your credit score?

Payment History: Paying your bills on time accounts for 35% of your credit score. It doesn’t matter what amount of payment was unaccounted for, it still counts negatively towards your score. From there, the score is based on how late the payment was and how often you miss future payments. It takes 24 months to restore the credit of one late payment.

Card usage/Amount owed: The next biggest factor is your credit card usage. Maxing out your credit cards is the #1 way to lower your credit score, along with not paying your bills on time. This factor is based on how much you owe on each account and how much of your credit you have used. When you are issued a credit card, you are given a credit limit. For example, if your credit card limit is $1,000, that doesn’t mean you should use all of the $1,000.

Credit History: The length of your credit history is the next biggest factor. Having a loan or credit card account for a long period of time is going to reflect positively on your score. Closing your actions too rapidly can cause your score to drop.

Types of Credit/New Credit: The types of credit you have and opening new credit are the last factors that affect your score. Always looking for new credit can add negative marks against your score. Lenders are looking at if you can open 1 or 2 credit cards, manage a few loans and maintain these things for a long period of time. Opening up new loans or cards in a short period of time may indicate overspreading your finances. This doesn’t reflect highly on your credit score.

Additional things that affect your credit score: borrowing from finance companies, having your credit inquired on more than 3 times in a year, or transferring balances of credit to another account.

What doesn’t hurt your credit score?

Debt ratio: The amount of overall debt between loans and credit card usage doesn’t add up collectively against your score.

Income: The amount of money you make doesn’t affect your score. Income may be a deciding factor in certain credit limits and perks, but it will never be used to calculate your score.

Length of Residence: The amount of time you have spent in a certain residence or owning property doesn’t affect your score.

Length of Employment: You don’t need to be employed for a certain period of time to create and build credit or open loans.

Criminal record and personal information: Any criminal records or personal information will not be used to calculate your credit score.

How to Improve or Rebuild Credit

720 is a good goal to have for your credit score, but what happens if you are far away from this number? Sometimes the need to improve or rebuild credit comes from a desperate feeling of wanting to change your score rapidly. There are many sources out there that claim they can build your credit fastor charge a fee for credit repair. Unfortunately, many of these sources are scams. The only way to rebuild and improve credit rely on behavior changes, resources, and time.

Over 70% of your credit score weight comes from the past 2 years alone, although some items can stay on your credit longer. This means you are not condemned to a life with low credit! It is totally fixable but you probably won’t see drastic changes to your credit score until about 24 months of active, good decision-making. Therefore, time is HUGE, be patient. During this time, you should be making a conscious effort to pay your bills on time, If you are going to close any credit cards– close them slowly, make payments on your loans, and only have 30% or less owed on any line of credit. This combined withtime will have you on the right track to a good credit score and may even increase your line of credit.

This may seem like a lot to do, but in reality, these things are spread out month to month. In the meantime, don’t over-monitor your credit score! It will drive you crazy. Trust that you are making the right decisions and check out reliable sources to help you keep track. Most importantly, beware of scams!

Who Can You Trust? What to Lookout For

When it comes to looking for reliable sources on credit, you may be bombarded with information. Overall, you shouldn’t have to pay to rebuild your credit or get additional information on how to manage your debt.

Who can you trust?

If you have one, your current bank or credit union

Annual Credit Report is a free site that you can use to always look up accurate credit scores

Stay away from credit repair clinics/sites and especially credit counselors that charge you money

Other Recommendations & Sources

Marine Credit Union makes managing your credit easy. Many of Marine’s members have credit education needs which makes us a leading resource in helping community members. Our employees at MCU are ready, educated, and willing to help you out with any of your credit concerns. Additionally, MCU has launched and revised our mobile app to offer digital banking in the palm of your hands. Not only is it convenient, functional, and easy, it also allows you to look at your FICO score fast and free. If MCU isn’t your current credit union/bank, talking to your current bank about credit options can be a beneficial start.

A lot of universities offer comprehensive guidance on campus for financial help like starting and maintaining credit. There are also state-wide resources on financial education that you can check out depending on your location. Credit building programs offered within your bank or credit union can also be very beneficial, like MCU’s Get Credit! If you don’t have a relationship with a bank or credit union, it will be crucial to start considering establishing one. We are here to help you, not harm your credit.

What a lot of people don’t realize is that you can contact your creditor directly with any concerns you have. Many people neglect the opportunity they have to communicate with their creditors about important situations like – telling them you need more time to pay your bills, needing a deferment, and just needing help in general. Don’t feel ashamed or guilty if you need help. Know that you are not alone, there are millions of people trying to get back on track and restore their credit. YOU’VE GOT THIS!

Maintaining your credit requires regular monitoring and proactive management. In this blog, you'll meet two friends, Oliver and Jesse, who take different approaches to managing…